Most pharmaceutical organizations do not struggle to explain what their AI programmes do. They struggle to explain, in financial terms, why those programmes deserve sustained investment.

That distinction matters more now than it did even a year ago.

In many pharma companies, the pattern is familiar. AI pilots generate interest. Teams produce compelling demos. Internal sponsors build momentum. Then the discussion moves from experimentation to investment, and finance asks a simple question:

What return should we expect, by initiative, over the next three years?

At that point, many programmes slow down.

Not because the technology lacks promise. Not because the teams lack ambition. But the AI strategy was built to prove technical potential, not to withstand financial scrutiny. The business case came late. The assumptions are broad. The costs are incomplete. And the link between AI capability and commercial outcome is more implied than modelled.

That is where many otherwise promising AI strategies fail the CFO test.

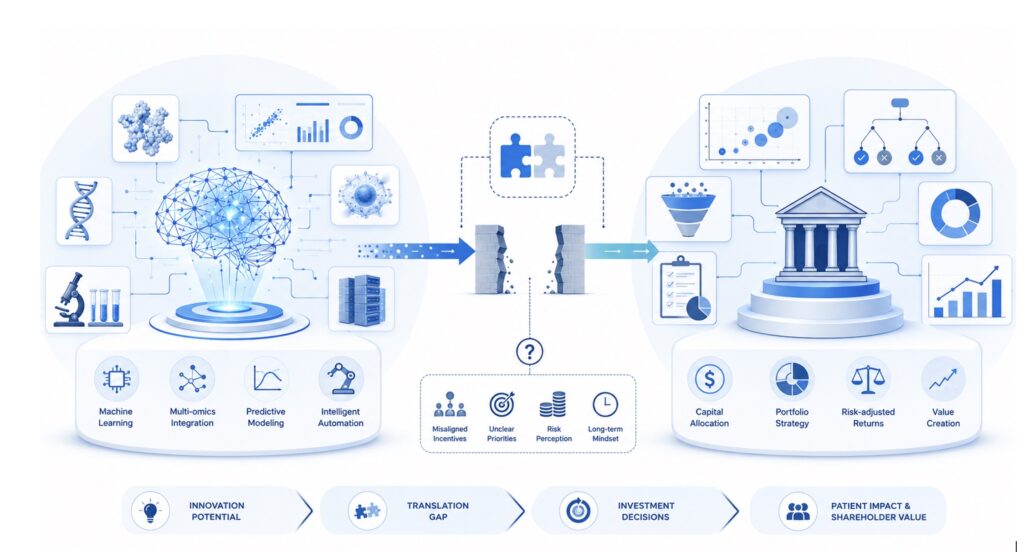

The Real Problem Is Not AI. It Is Investment Logic

Most AI programs enter organizations through innovation teams, data science functions, or vendor-led pilots. That shapes how they are discussed internally. The early focus is usually on capability: what the technology can do, how fast it is improving, and where it might be applied.

That is reasonable at the exploration stage. But it creates a structural problem later.

AI often arrives with innovative logic. CFO approval requires capital-allocation logic.

Those are not the same thing.

Innovation logic asks:

● Can the technology work?

● Where might it help?

● What should we test first?

Capital-allocation logic asks:

● Which initiatives create measurable value?

● What assumptions drive that value?

● What will it cost to implement and operate?

● When will returns appear?

● What risks could erode those returns?

● Why should this be funded before something else?

Many pharma AI programs are still trying to answer the second set of questions with material built for the first.

That is why a successful pilot so often fails to become a scaled investment decision.

Why Has This Gap Become More Serious

For a while, organizations could afford to treat AI as exploratory. A promising proof of concept was often enough to unlock a limited budget. The financial stakes were low, and the strategic upside seemed worth testing.

That environment is changing.

Pharma leadership teams are under greater pressure to justify investments with greater precision. Growth is harder won. Major products are approaching or entering loss-of-exclusivity periods. Budget holders are being asked to defend not just whether an initiative is interesting, but whether it is financially superior to competing uses of capital.

In that environment, AI does not get special treatment.

If anything, it gets harder scrutiny. The excitement around AI has raised expectations, but it has also raised the standard of proof. Senior decision-makers increasingly want to know not just whether AI can create value, but where, how much, how soon, at what cost, and under what conditions.

That requires more than enthusiasm, benchmarks, or pilot results. It requires a financial model.

What a CFO Actually Needs to See

A credible AI business case in pharma is not a slide on productivity gains. It is not a vendor proposal with projected upside. And it is not a portfolio of use cases accompanied by broad ROI estimates.

A CFO needs something more rigorous: a model that connects AI investment to business outcomes through explicit assumptions, initiative-level economics, and realistic scenarios.

In practice, that means five things.

1. A clear link between AI and the decisions that drive value

The strongest AI business cases do not start with use cases in the abstract. They start with the decisions that matter most to business performance.

In pharma, those decisions may include:

● field force prioritisation

● HCP engagement strategy

● market access evidence generation

● demand forecasting

● patient identification

● medical affairs workflow decisions

● portfolio and pipeline prioritisation

The key question is not simply where AI can be used. It is where AI can improve the quality, speed, or consistency of decisions that directly affect revenue, cost, risk, or time to value.

This matters because technical performance alone does not create financial return.

A model that predicts HCP behaviour accurately may be impressive. But its value depends on whether the insight changes commercial action, whether teams adopt it, whether workflows support it, and whether the resulting impact can be measured in financial terms.

That causal chain must be explicit. Without it, the financial case is little more than extrapolation.

2. Initiative-level financial modelling, not programme-level averages

“AI ROI” is usually too blunt to support serious investment decisions.

What finance needs is a view by initiative: expected cost, timing, benefit, dependencies, and risk. Which initiatives produce fast returns? Which requires more enablement? Which creates strategic capability but limited near-term payback? Which look attractive in theory but do not materially affect the P&L?

This level of detail improves decision quality in several ways.

First, it makes prioritisation possible. Leaders can distinguish between strategically interesting initiatives and those that are financially meaningful.

Second, it supports better sequencing. Some initiatives generate early value. Others depend on capabilities that have to be built first.

Third, it prevents a common problem in AI strategy: weak initiatives hiding inside strong portfolio averages.

A programme-level ROI number can make a portfolio look attractive while concealing the fact that some initiatives are unlikely to justify the investment. Initiative-level modelling makes those trade-offs visible.

3. Explicit assumptions about adoption, workflow change, and redeployment

This is where many AI business cases become optimistic.

A model often assumes that if AI saves time, value has been created. Finance does not see it that way, and rightly so.

Time saved is not the same as financial benefit.

If an AI tool reduces effort in a given process, the real economic question is what happens next. Does the organization redeploy that capacity into higher-value work? Does it remove cost? Does it improve throughput? Or is the time simply absorbed without a measurable financial effect?

That answer varies by function, process, and timeframe. Which means the financial model has to be specific.

The same is true for adoption. Many AI cases assume usage will be high because the tool is capable. In practice, value depends on whether teams trust it, workflows incorporate it, incentives support it, and managers reinforce its use.

A model that projects large returns without explicit assumptions on adoption, workflow change, and redeployment is not robust enough for board-level scrutiny.

Or more simply: if the model shows time savings but does not show what happens to the time, it is not yet a financial model.

4. The full cost of operating AI at scale

Many business cases understate the cost side because they focus on licences or initial build costs.

That is rarely enough.

A serious model should include the full operating picture:

● software and model costs

● implementation and integration

● data engineering

● validation and testing

● training and change management

● governance and compliance

● monitoring, maintenance, and support

● vendor management

● security and risk controls

This is especially important in pharma, where governance, compliance, and operating discipline are not optional add-ons. They are part of the real cost of scaling AI.

It is also important because AI cost structures are still evolving. Consumption costs, enterprise pricing models, and platform choices can materially change the economics over time. If the model assumes those costs remain flat, that assumption should be visible and stress-tested.

Finance does not expect perfect certainty. It does expect honest cost accounting.

5. The cost of delay, not just the cost of investment

A strong AI business case should not only model the upside of investing. It should also model the cost of moving too slowly.

That is often missing.

In many organizations, the comparison presented to leadership is between investing in AI and not spending the money. But that is not the real choice. The real choice is often between building capability now or accepting a weaker competitive position later.

Delay carries costs.

Organizations that move earlier tend to build:

● better data readiness

● stronger governance capability

● Greater organizational fluency with AI

● more practical knowledge of where AI works

● faster implementation muscle

● a more realistic understanding of cost and value

Those advantages compound. The later an organization starts building them, the harder they are to close quickly.

That does not mean every AI investment should be rushed. It means the “do nothing” scenario should not be treated as neutral.

The Hidden Financial Lever Most Organizations Miss: Sequencing

One of the most important outputs of rigorous AI financial modelling is sequencing.

Most pharma organizations still evaluate AI initiatives as though they were separate decisions. A use case is reviewed on its own merits. Another is assessed in parallel.

A portfolio is assembled from the initiatives that appear individually strongest.

On paper, that sounds rational. In practice, it often produces a weak programme.

AI initiatives are rarely independent. Their value is shaped by what exists around them: data quality, workflow integration, governance, user adoption, operating processes, and the ability of teams to act on the output.

That means order matters.

Some initiatives should come early because they build foundational capability. Some should come early because they generate returns that can support later investment. Some should wait because, without the right infrastructure or behavioural change in place, their projected ROI will not materialise.

This is where many strategies leave value on the table.

An initiative that looks only moderately attractive in isolation may become highly valuable once the right data, workflow, and adoption foundation exists. Another that appears compelling on a standalone basis may underperform if launched too early.

So the question is not only which AI initiatives should we fund? It is also in what order should we fund them to maximise total return?

That is a much more strategic question, and a much more financially useful one.

What Changes When the Financial Case Is Built Properly

When organizations build an AI strategy on a stronger financial foundation, the benefits go beyond the spreadsheet.

First, the board conversation improves.

Instead of asking leadership to endorse AI as a broad strategic direction, the organization can present a clear investment case: these initiatives, this sequence, these costs, these assumptions, these expected returns, these risks. The conversation becomes more disciplined and more productive.

Second, alignment improves across functions.

Commercial, finance, technology, operations, and compliance teams often talk past one another when AI strategy is framed too loosely. A shared financial model gives them a common language. It makes trade-offs visible. It forces assumptions into the open. And it reduces the amount of decision-making driven by internal enthusiasm or politics.

Third, execution gets faster.

Paradoxically, more rigour at the front end often speeds things up. When the logic of the programme is clear, organizations spend less time re-arguing why an initiative matters and more time implementing the ones that do.

A Simple Test for Your Current AI Strategy

There is a straightforward way to tell whether your organization has crossed from AI activity into AI strategy.

Ask this:

If the CFO asked tomorrow for the projected financial return of each major AI initiative, by year, over a three-year horizon, with explicit assumptions for adoption, operating cost, and redeployment, could the organization produce an answer that would survive scrutiny?

If the answer is yes, the strategy is on stronger ground.

If the answer is, “we have something directional, but not something finance would rely on,” that is the real gap to address.

Not model sophistication for its own sake. No more pilot activity. Not a more ambitious AI narrative.

A stronger financial case.

The Organizations That Will Lead Will Be the Ones That Can Prove Value.

The next phase of AI in pharma will not be defined by who ran the most pilots or signed the most technology partnerships.

It will be defined by who built the discipline to connect AI investment to measurable business outcomes, with enough precision to guide real capital allocation.

That means knowing where AI creates value, what assumptions that value depends on, what it costs to deliver, which capabilities need to come first, and how quickly returns can be realised.

In other words, the winners are unlikely to be the organizations with the most AI activity.

They are more likely to be the ones with the clearest financial logic.

And increasingly, that is the standard the CFO will expect before approving what comes next.

Conclusion

The organisations that lead the next phase of AI in pharma will not be the ones with the most pilots. They will be the ones with the clearest financial logic – initiative by initiative, cost by cost, return by return, against each other.

Found this article interesting?

If that is the gap this article has surfaced, the Eularis Board-Defensible AI Strategy Blueprint is built to close it.

In 3-4 months, (depending on client scope) personally directed by Dr. Andrée Bates with a multi-functional team of senior specialist leaders, the Blueprint delivers what no vendor-led assessment or internal working group produces on its own: a comprehensive AI strategy across the full enterprise, with detailed financial modelling for every priority initiative, rigorous vendor-neutral analysis, a governance framework aligned to the EU AI Act, and board-ready materials your leadership can actually present and defend.

It includes a two-day Dr. Bates-led executive offsite to align your leadership team – and the option for an ongoing advisory relationship beyond the engagement.

Capacity is constrained.

The CFO test is coming. The Blueprint is how you pass it.

For more information, contact Dr Andree Bates abates@eularis.com.